Hi everyone, welcome back. As mentioned in the last blog post, I conducted a survey at the start of September to get an idea about what my friends felt about food security.

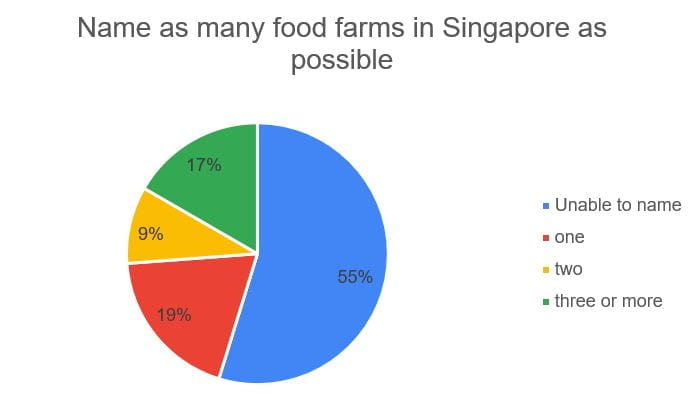

I realised that most respondents were not too familiar with the various local farms in Singapore. I asked respondents to list as many food farms as possible and vetted through their answers.

Most people could not name specific farms (although they were aware that Kranji/Lim Chu Kang had some and that there were fish, poultry and that one goat milk farm). This shows that the brand recognition of our local farms isn’t that high.

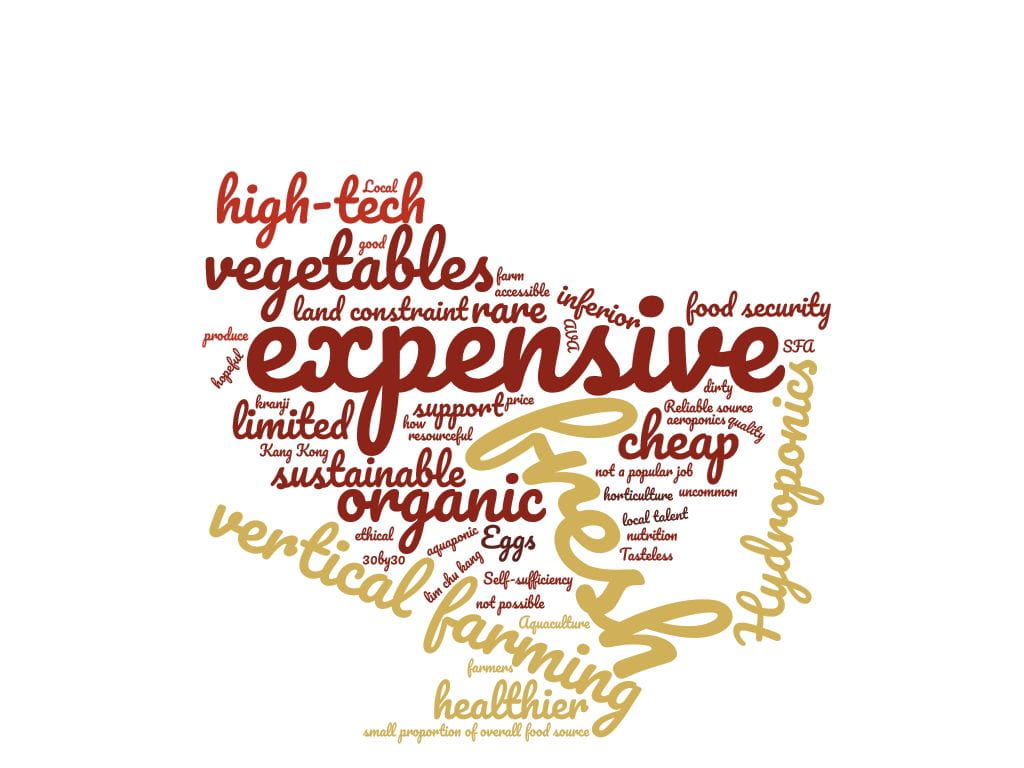

I looked back at the word cloud shown in last week’s post and realised that both “cheap” and “expensive” were commonly associated with local produce. I decided this warranted another survey and expanded the target audience to family and my hallmates.

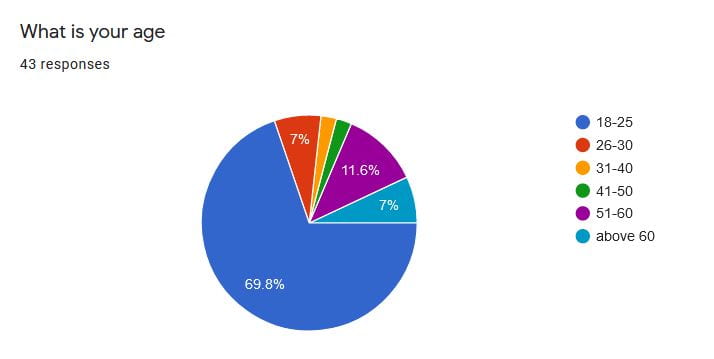

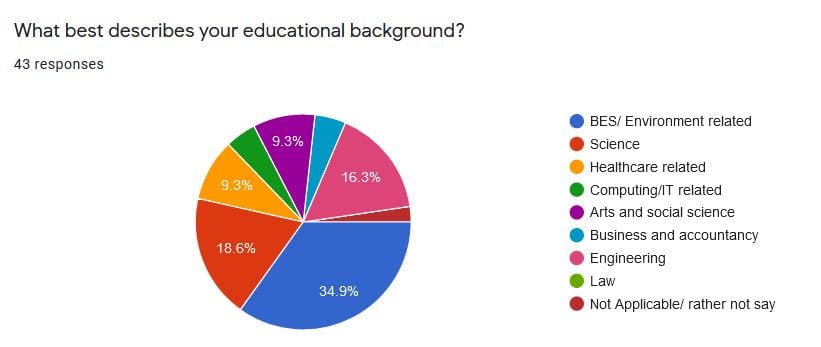

Here is the breakdown of the demographics:

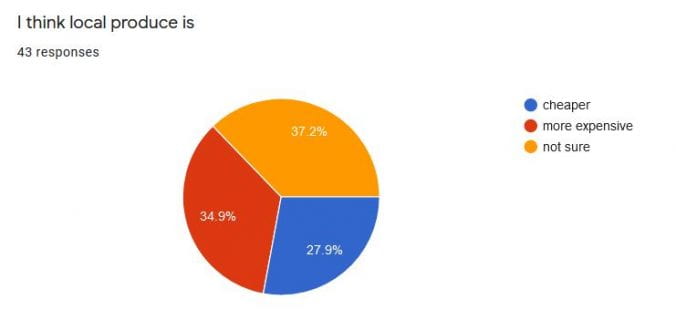

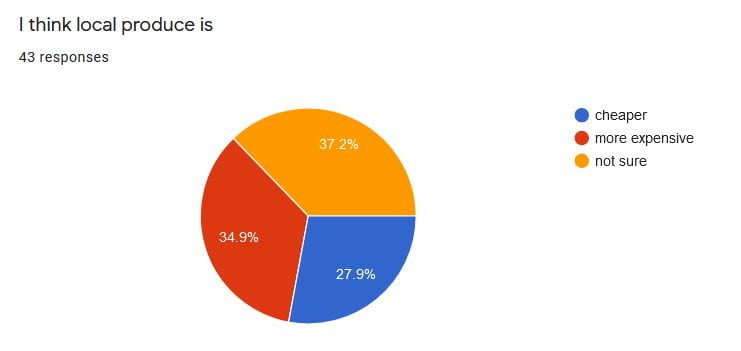

I asked respondents if they thought local produce was cheaper or more expensive. It appears that most of us were not sure, but fewer people thought that local produce was cheaper.

I avoided phrasing it as a agree/disagree question so as to not influence their answer, but “I think local produce is not sure” doesn’t make sense haha

Is this really the case? As mentioned in the last post, NTUC Fairprice carried more local produce than other supermarkets online. I compared local produce types on NTUC with imported produce from NTUC, Sheng Shiong and Red Mart, selecting the cheapest option for both local and imported produce, ignoring temporary offers. Here are my results:

| Item | Domestic

($/100g) |

Imported

($/100g) |

Cheaper option | % difference from imports |

| Bean Sprouts (taugeh) | 0.35 | 0.38 | Singapore | -7.9% |

| Xiao Bai Cai | 0.41* / 0.56 | 0.40 | Malaysia | 2.5%/40% |

| Kow Peack Cai/ Jiu Bai Cai

(Not sure if this is a Bai Cai variant similar to Xiao Bai Cai) |

0.40 | NIL | NA | NA |

| Baby Kai Lan | 0.63 | 0.78 | Singapore | -19.2% |

| Cai Xin variants | 0.41*/ 0.57 | 0.40 | Malaysia | 2.5%/42.5% |

| Round Spinach | 0.41* | 0.38 | Malaysia | 7.9% |

| Barramundi | 4.33 | 3.90 | Vietnam | 11.0% |

| eggs | 0.40 | 0.27 | Malaysia | 48.1% |

Prices marked * are Pasar brand vegetables that are primarily sourced from Singapore but may use Malaysian produce to meet shortfalls. There is no difference in price between the local and Malaysian variants. I have included the next cheapest SGFP certified alternative if available.

Taugeh was a shoo-in and I struggled to find imports for that. It turns out that 70% of taugeh is grown locally. While our barramundi may be more expensive, we have a surprisingly large number of suppliers of fresh and frozen versions. While the price difference in eggs may appear significant, this was because local brands did not carry the larger 30 – egg trays and most chose to differentiate themselves in terms of freshness and nutritional value. If local egg farms are aiming to portray freshness, it may not make sense to sell the larger variants at supermarkets that may take longer for the average consumer to finish. I suspect they do sell in bulk to stall owners instead. Moreover, at the point of writing the cheapest local egg sold is actually on discount at $0.35/100g (29.6% more expensive than imports) while being lower in cholesterol with added Vitamin E.

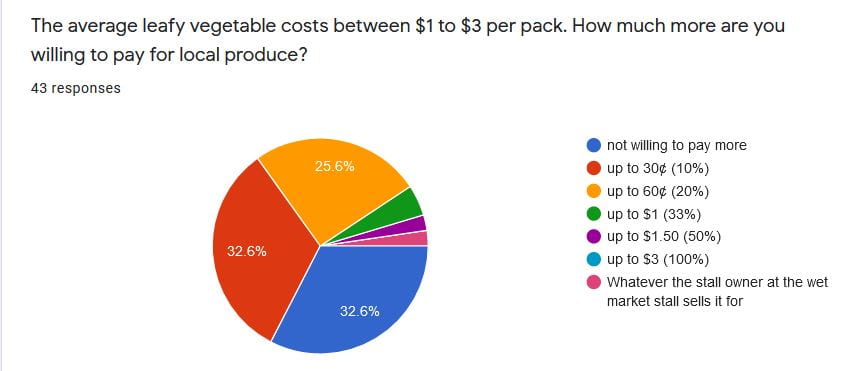

While there are cheaper imported leafy vegetables, the price difference is minimal. In fact, more than two-thirds of respondents were willing to pay up to 10% more for local produce.

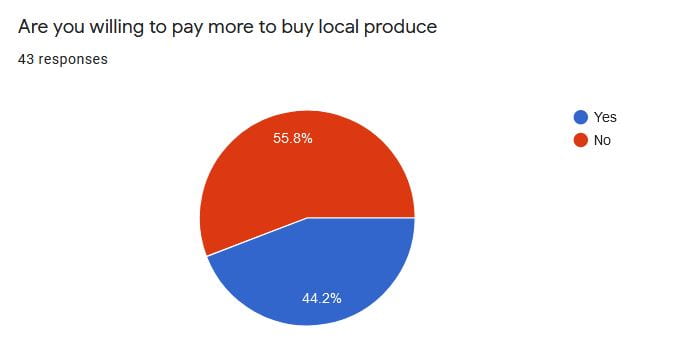

What’s interesting is that originally 44% of respondents were in principle unwilling to pay more before I quantified the price difference.

So, while local produce may not necessarily always be cheaper, the price difference is minimal and may be made up by the difference in quality such as freshness.

As we can see, when it comes to food, price is not the sole determinant. In conclusion, local produce can be competitive with imports even at the current price levels.

Through the course of these two posts, I’ve identified a few limitations with the SG Fresh Produce scheme. I’d be wrapping up this “trilogy” next week!

Cheers,

Ee Kin

Recent Comments