I still love eating – who doesn’t? After 11 weeks of looking at the food production scene in Singapore and beyond, I have come to appreciate many tiny details along the way.

It was interesting to see how this topic of food security touched on what I have learnt this semester – not just in ENV1101. From the SG Fresh Produce logo invoking Geographical Imaginations under the Singapore brand to price elasticity and its effects on our imports. All the research I did for this blog really opened my eyes to certain quirks of food production – from what vegetables were produced to even less conventional ways produce were sold and the considerations of producers.

Your questions and comments also challenged the way I think and write, from exposing certain blindspots or highlighting areas where my choice of words made what I was trying to portray ambiguous. Amidst this COVID pandemic, many of our interactions were online and all our earlier interactions in the comment section in each other’s blogs did help foster a stronger sense of belonging and familiarity within the BES community for our batch. I look forward to meeting everyone “IRL” next sem.

collab on frog legs. A 14-year journey from farm to fork – and meeting new people along the way

Of course, there are many aspects of this blog that could have been done better. The visual attractiveness of this blog being the most noticeable at first glance, as well as how I display information from interviews and the overall structure of my blog. There are still some topics that have not been covered – such as what lessons we can learn from our water security story as well as more on the impact of our 30×30 goal beyond Singapore. Here are some blogs that are presented very differently from mine that may interest you: Sherry’s was highly structured and well thought out from the beginning, Natasha’s was a lot more visually appealing and this post by Kelly really incorporated interesting media. I should probably have experimented with and adopted their best practices earlier, especially after I realised I have the creativity of a peanut…

A word of advice to any juniors reading this in 2021 and beyond: choose a topic you are interested in then think about how that affects the environment. Suprisingly, I managed to include many of my other “random” interests from numismatics to scouting and gardening (either that or I was actually shoehorning unrelated stuff in, you be the judge). If your area of interest seems to already have been covered by the seniors, how have your lived experiences influence how you view the same issues?

Oh, it is also important to think critically when reading other’s posts. For example, my advice in the previous paragraph may actually be a bunch of hogwash.

update on my tomato seedling – transplanted it a bit late but it has grown a lot over this semester too. Draw whatever metaphors you want.

That’s it from me. All the best for finals and good luck (and have fun) on your blogs if you’re reading this in the future. Spare a thought to where your food comes from and how sustainabe they are!

Hi everyone, welcome back. Last week, I was part of the World Organisation of the Scouting Movement (WOSM) team that took part in the takeover of the UN Youth Envoy’s social media accounts.

WOSM’s takeover of the UN Envoy on Youth, retrieved from https://www.instagram.com/p/CG4_0JjDrQn

I chose to talk about food security amidst global warming, and this comprised Instagram Stories as well as a written opinion piece.

I was quite apprehensive at the start – after all, I am just a year one BES student with seemingly no experience. However, I was encouraged to look at personal stories. I soon realised that many small decisions I made many years ago, and all the “random” activities I took part in have shaped my world view now. Some may call this lived experience. Personally, choosing to continue with the “germinating taugeh” experiment in primary school and repotting it blossomed into a love of gardening and nature.

This was probably reinforced by all the hiking in nature parks my family did in Hong Kong when I was a child and my experience as a scout. All these ties in pretty closely to the chart we will see in this week’s notes (slide 60) about building environmentally literacy.

In my op-ed, I espoused community gardens as a means to increase awareness of food security – a more personal touch of sorts. To an extent, gardening may already be quite popular here. All of the plots in older allotment gardens are fully subscribed, so people are willing to pay to garden. In fact, community gardening is the raison d’être of the social enterprise Ground Up Initiative. While I acknowledged that there are people who use these gardens to supplement their diets and increase their food security, I may have missed a much larger impact of urban farming. According to this article, urban farming could also improve relations between stakeholders, increase cities’ livability and even provide job opportunities. While the “Gardening with Edibles” programme proclaims its support for the “30by30” goal, the unrequited love on SFA’s part is puzzling. Surely this is a good opportunity for outreach?

When researching for the op-ed, I also came across measures such as growing on rewetted peatlands that our neighbouring countries could take that may be carbon neutral while ensuring food security. Given the more inward-looking aspect of “30by30”, I wonder if this may translate to reduced support for sustainable solutions overseas. The “diversify imports” strategy also means that breadth is valued over sustainability. When it comes to national security, sustainability may have to take a back seat. Given climate change’s varied effect on global food production, importing food from beyond our region hedges our bets but ironically becomes a positive feedback loop. Environmental justice would also be a greater concern if global food shortages see even more food imported out of already impoverished regions. This is not a new concept and nobody wants a repeat of the 1943 Bengal Famine.

Taking part in this social media outreach highlighted the global nature of some local problems. After all, even if “30by30” is a resounding success we would still need to account for the remaining 70%. Collective action needs to be taken on what is essentially a collective responsibility. Every member of society can do their part.

Hi everyone, welcome back! So far, we’ve been looking at the 30by30 goal and how it would affect food production in Singapore in the immediate future. But what about beyond 2030? Will it be a high tech (u/dys)topia, and what role would more conventional farms play?

As Alicia mentioned in her post, cell-cultured meat products such as Shiok Meats are gaining attention. In a recent press release, they claim that cultured meat may reduce “greenhouse gas emissions by 96%, energy consumption by 45%, land use by 99%, and water consumption by 96%”. This is supported by various journal articles. Reading through them, I realised that not all cultured meat will save energy as livestock like poultry are conventionally less energy-intensive. For Shiok Meats, I am not sure if the savings will be as high compared to other local high tech farms in operation. Local shrimp farm Universal Aquaculture employs closed system vertical farming which reduces water consumption – unlike Shiok Meats which is still in the R&D phase, they plan to produce 400 tonnes by 2022.

So how do companies like Shiok Meat plan to capture the market share? In an interview with Channel News Asia, the co-founder shared that they plan on equipping existing farmers with the technology once it is commercially viable. This makes a lot of sense as these farmers are already well integrated into the supply chain. While cultured meat has not been able to replicate the full animal yet, they might be able to meet the demand for processed food similar to HaiDiLao’s popular smashed shrimp paste.

But would the public accept cultured meat? Only a quarter of my survey respondents were open to giving it a try.

plant-based “fake” meats seem most popular

I think some hesitation stems from it being unnatural and seen as “lab-grown” – in fact, the way I phrased the option may have led some to view it negatively. On a commercial level, cultured meats will be produced in facilities more similar to food processing plants than labs. More people may be concerned about the safety and ethical implications of the award-winning TurtleTree Labs, which produces breast milk. It can be harder to trace the origins of cultured animal products, and some people may be put off by the idea of producing human products the same way as other common livestock.

took part in a taste test for “pork” dumplings. They were…ok

Does this mean that the future of local food production will solely be in cultured meat with no conventional farms? I don’t think so. Cultured meats require culture mediums – and it would be great if the nutrients could be derived from local vegetables and produce. As mentioned earlier, poultry farming tends to be less resource-intensive and it may not make economical sense to culture chicken meat. Another aspect would be more “niche” meats – such as frog meat which I tried with Anna recently (read her blog here). After interacting with patrons, I realised that while there is always a demand for frog meat, it might not be enough to justify the R&D into making cultured frog meat. Just with organic or non-GMO produce, there will always be a market for “conventionally” farmed meat too.

That’s all from me, join me next week as I bring this to a close and look beyond our shores.

“Be woke and conscious about how we can all be more sustainable and live in greater harmony with nature.”

– James Kwan, Chief Marketing Officer, Barramundi Asia

Hi everyone, welcome back. While we have examined the 30by30 plan so far, this has been mostly from the viewpoint of a consumer. There may certainly be blind spots we don’t know about, and nothing beats the experience in the industry. On the 12th of October, I had the privilege to interview Mr James Kwan, Chief Marketing Officer of Barramundi Asia. Barramundi Asia is the parent company of Kühlbarra – a local barramundi farm – and UVAXX – which oversees fish health.

Here are the highlights of our interview as well as my thoughts. The transcript of our phone interview can also be found here.

Q: Your farm is currently the only one situated in deeper waters. Why has Barramundi Asia taken this unique approach, and why isn’t this more common?

A: In South East Asia, the traditional and primary form of aquaculture production has largely been kelongs. While kelongs are tried and tested, and suitable for artisanal volumes; intensive aquaculture requires deeper ocean waters with strong currents to ensure low stocking densities and disease mitigation and ultimately healthier, and happier fish. For Barramundi Asia, we have adopted methods from the global industrial salmon aquaculture for barramundi, where we use large and deep sea cages…(depths of around 20 metres and a diameter around 25-30 metres). These nets allow large volumes of water, and when carefully stocked with the correct biomass, are optimal for growth and animal health. This mode of aquaculture is typically more capital and investment heavy, as they require surface support and harvest vessels, floating living quarters, feed storage, dive operations…etc, which is probably why we are one of the few in Asia that adopt this method.

Q: Are there any concerns about water quality given your open net system? Are harmful algal blooms (HAB) a concern?

Water quality in aquaculture is always a priority and challenge, whether you are culturing in a land-based pond, lakes or in shallow-based kelongs or out in the open ocean. This is precisely why as a farm we sited our farm in the southern waters of Singapore because of the strong oceanic currents. There are multiple environmental factors that make HAB events more likely…by situating our farm in waters that have strong currents, high dissolved oxygen readings, and away from potential agricultural nutrient pollution sources and outfalls, we mitigate these risks significantly. I distinctly remember the afternoon in 2015 when our northern farms along the Johor Strait experienced a HAB that wiped out 600 tons of fish biomass; I was diving a cage with a prominent local French chef who had dropped by to see how we farmed in deep waters. We talked about the importance of surveillance and HAB forecasting, so that farms are able to be prepared for any eventuality. Unlike kelongs, we could technically un-moor our cages and tow them away from affected waters if necessary.

Apart from the measures mentioned, I think that it is also important that SFA works with industry players to seek their input and experience when it comes to formulating guidelines and licensing agreements. With the rather nascent aquaculture scene in our southern waters, farm operators would have the most experience when it comes to on-site conditions. Taking the more crowded northern waters into account, factors such as oxygen demand should be considered in the future. These operators also stand to benefit from being able to have their voices heard. While some people may be suspicious of any cooperation between the government and corporations, I think that the knowledge industry players bring is irreplaceable. Of course, there is always space for evidence-based policymaking through studies of site conditions, but that may take a bit more time and research funds.

Q: Why did your company choose to specialise in Barramundi? I notice that Kühlbarra also offers salmon. Are there plans to farm other fish?

A:There are many reasons why barramundi was chosen. As we are situated in the tropics, we had to find a viable species that would meet the requirements of fast growth, disease resilience, optimal feed to protein conversion, and market acceptance. Barramundi (sp. Lates calcarifer) is particularly suitable also because it can be acclimatised to pellet feed. where we are able to then tailor nutritional and sustainable components to the feed. The feed that we use is 70% plant base, with a very low FCR (feed conversion ratio), which ultimately makes our barramundi, arguably the most sustainable premium white fish in the market.

We sell salmon on our online store as an added value-add to our customers who may also want salmon. Many of our management team come from the salmon aquaculture industry and have strong ties with producers around the world, allowing us to bring in fresh salmon regularly.

I think this is really eye-opening. It is great that the fish can be fed pellets, which are less pollutive and less likely to spread disease as compared to other methods such as trash fish. The use of vegetable proteins as opposed to the meat or fish-based ones also mean a lower carbon footprint, making it more sustainable overall.

Q: It is estimated that half of your production is sold locally while the rest is exported. Is local demand not high enough, or are there other benefits to exporting your products?

A: As a business, we need to look into all markets to ensure financial sustainability. But as Singapore’s largest aquaculture producer, we of course prefer to focus on local demand.

While the market can absorb more fish from our farm, we offer a product that is produced towards the highest standards and that obviously comes with a cost. We are one of a handful of BAP( Best Aquaculture Practice) certified facilities in the region; and the only in Singapore. We use only 100% traceable, sustainable feed, monitor our water quality and maintain assure customers of 100% chain of custody of our fish from farm to fork. So while we see more local consumers beginning to demand for better quality, certified farmed fish, the volume we produce is sold offshore to more developed markets where customers only want traceable and sustainably produced fish.

For example, in Australia, our farm in Western Australia produces fish that are sold to Coles supermarket chain, with around 800 stores around the country. In the US or across certain international hotel chains, our products are selected because we are able to produce to the standards required. In Singapore, you can find us in Cold Storage, RedMart or through our online portal at kuhlbarra.com.

As shown in my survey results from the previous post, Singaporeans are not just price-conscious but also pay attention to taste and quality. It is logical for local farms to focus on their freshness and taste – and it has evidently served Kühlbarra well. It might also be harder to compete with cheaper fish from less sustainable farms in the region. Anecdotal evidence in the comments section suggests that there is some baseline level of demand, even if they may be more pricey.

Image by Eleanor Loh/ Steamed Tiberias Barramundi from the Open Farm Community. Personal photograph reproduced with permission.

I’ve tried locally farmed barramundi at the Open Farm Community restaurant, and it tasted pretty good. However, at that price point if we weren’t there for a celebration I may not have gone. With the recession caused by the COVID pandemic, people may become more price conscious too.

Q: Your products are vacuum sealed for freshness and delivered in styrofoam boxes. How will the Resource Sustainability Act affect you and what measures are being considered to reduce waste?

A: As our business extends past just aquaculture and into fish and food processing, we are very much committed to working towards zero waste solutions. However, as we mainly deal with a fresh product, we do need to rely on IVP (individually vacuum packaging) to ensure food safety. We transport some of our products in EPS boxes to ensure cold-chain integrity for food safety. Despite the limitation of Expanded Polystyrene (EPS) densification and recycling facilities within Singapore, we believe that EPS’ benefits far outweigh its cons in terms of its insulative performance. To mitigate this, we do have a return policy for our polystyrene boxes where the delivery agent retrieves it during the next delivery. Recycled boxes are brought back to our factory and disinfected with food grade alcohol. We are also exploring hybrid paper based IVP primary packaging, working with international customers on their requirements. At the end of the day, it is a multiprong strategy that involves our customers too.

In terms of sustainability and waste management, we are also looking at employing ensilage systems in 2021 to ensure that food trimmings, mortalities and other biological waste are treated within our own company, with end products potentially sold downstream to feed or fertiliser companies.

Now, this is where the 30by30 goal may not necessarily bode well for the environment. By emphasising freshness, certain single-use packaging may come into play. How many people would be willing to have fish delivered in an insulative box and handed over without any packaging? As I learnt during an online seminar on the Resource Sustainability Act, vegetable farms also grapple with the issue of plastic packaging for veggies delivered to supermarkets. It would be interesting to compare that with groceries bought from neighbourhood markets, where fish and vegetables are displayed without packaging. If anything, producers may be responsive to consumer feedback when it comes to packaging.

Once again, I’m thankful for James to take the time for the insightful interview and to his team for vetting through the transcript.

We talked a lot more – which I do not have the space to elaborate on. It’ll be appended at the end for your perusal.

Cheers,

Ee Kin

Q: Has COVID-19 affected your plans to triple production by 2022?

A: Definitely all farms around the world are affected. For us, as travel restrictions came in place and the Aviation and HORECA (HOtels, REstaurants, CAtering) industry got devastated, so did B2B orders for our fish. Thankfully, as we have a relatively robust online presence well established, and a loyal following, we saw an uptake in our online sales by over 3x as the Circuit Breaker came in place. Despite this, we have made the necessary changes in our business and production to meet our 2022 volumes despite the severe impact of COVID.

Q: How does the 30by30 plan to increase food production affect you? Are there areas in current measures that you feel could be improved on?

A: As a Singaporean company with global ambitions, we believe and fully support the government’s initiative towards our 30×30 Food Security goals. It doesn’t affect us per se, but in fact has spurred our team on as we believe that Singapore, as unlikely as it is, can be a global aquaculture player, and a country that can further strengthen our already strong food security framework. It is fantastic that more Singaporeans are now aware of the importance of supporting local produce, which has been put in the spotlight during Covid.

For the SG produce logo, I remember voting for my preferred design earlier this year. I think it is a great start to start branding and recognising al local farmers. Perhaps apart from informing Singaporeans about the existence of a vibrant local food production sector, it hopefully inspires more of our young Singaporeans to participate and join this exciting sector.

Q: How do your Kimberly site in Australia and the upcoming site in Brunei benefit food production in Singapore?

A: Recently, the government has highlighted this through the “game change food security” advertisements. I believe we are the only Singaporean company that has taken production abroad. The government has supported us tremendously and we believe in their vision that food security and production need not be constraint to within national borders. By investing in Singapore companies that can produce outside of our shores, we add an additional dimension and strength to an already strong Food Security framework.

authors note: Check out SFA’s website on the latest updates on the Grow Overseas strategy.

Q: Can you comment on the relations with other fish farms in Singapore? Is it a close-knit community or do farms generally operate independently?

A: Farmers do operate independently, and are still loosely associated in Singapore. In the coming years, we hope to see greater interaction. Of course, we would like to think we have a great relationship with all other farmers! (laugh). Farming is somehow a primal activity and that alone makes us more understanding and sympathetic to one another’s challenges. As the largest and most resourced farm in Singapore, we do want to share or expertise and experience with those who are willing to listen. However, as our method of production with large ocean nets and deep waters are different from every other farm in Singapore, I guess there is knowledge that are not quite transferable. At Barramundi Asia, we are not just farmers, but a congregation of marine biologists, animal health and husbandry specialists and veterinarians. So we do feel for every other farmer, say when they were hit by the HAB in 2015. As an animal lover, we were all sick to the gut when we realised how many animals were affected. Recently, as part of our CSR and efforts to give back to the industry, our wholly-owned, sister company and hatchery, Allegro Aqua, just donated fingerlings to a farm in the north. We also sell this fast growing fry and fingerlings that are disease-resistant to other farms. An ST journalist was present and I believe it will be covered by the Straits Times soon.

Q: Is there anything else you want to tell our readers?

A: It’s important to eat local, support local. Know what you are eating….know what went into the animal you ate and how it was farmed and harvested. Be woke and conscious about how we can all be more sustainable and live in greater harmony with nature.

Hi everyone, welcome back to the last instalment on SG Fresh Produce. I’ll be moving into a case study of sorts next week. As mentioned previously, this post will be about the limitations of the SG Fresh Produce scheme.

SG Fresh Produce logo

Starting off with the SGFP logo, not everyone liked it as much as I did.

The bulk of respondents were actually rather indifferent. I probably should have followed up asking if people will find this logo effective

The bulk of respondents were actually rather indifferent. I probably should have followed up asking if people will find this logo effective

Many people who did not like the logo disliked that the focus was on the “SG” component rather than on the freshness or that it was specifically farmed in Singapore. As mention in the previous post, I suspect this may have something to do with the overall SG Branding. I wonder if the target audience is not just the local population, but also customers to markets we export to. We do export some livestock to countries as far as Australia and the US. The relevant agencies would, of course, try their best to improve the perception of local products in the global market, including that of primary produce. Personally, I don’t think this interferes too much with the logo’s main aim to raise help shoppers to identify local produce. With the big “SG”, I doubt anyone would be mistaking it for imported produce anytime soon.

Another limitation of the SG Fresh Produce scheme is that it only applies to primary produce. This limits us to uncooked, unprocessed food.

The bulk of my respondents do not personally use primary produce on a weekly basis.

The bulk of my respondents do not personally use primary produce on a weekly basis.

Just think back to the pre-COVID days, most of us patronised canteens/other cooked food stalls for lunch instead of bringing food from home (and of course there were those of us who did not need to worry about buying groceries as the government so kindly looked after these needs for two years). In fact, approximately a quarter of Singaporeans eat out daily.

But how can cooked meals be certified as being more locally produced? We certainly cannot have a fully locally produced meal – we don’t grow most of our carbohydrates to start with. In fact, the varied origin of our food has already been noted during the debate on the Geographical Indication Act (2014).

“For Katong laksa to qualify… the laksa leaf would have to be a Katong laksa leaf, the rice flour (used) would have to come from rice grown in Katong and the taupok (soya bean puff) would have to come from the soya bean that was grown in Katong. The clams would have to be harvested there as well”

– Ms Indranee Rajah, then Senior Minister of State for Law

Perhaps a separate certification scheme could be in place for cooked food that just looks at the origin of vegetables and proteins used. After all, there are already some F&B outlets that market themselves as being more conscious in terms of using local produce.

Of course, for the certification scheme to be successful, there must be demand for F&B outlets using local produce. Just slightly over 10% of respondents indicated that this would have any bearing on whether they supported a store. The main reasons for supporting would be taste – which may be tied to freshness – and price.

In the end, we are a rather practical bunch. In the end, we do prioritise convenience and price if taste is taken out of the equation.

only one person surveyed would patronise an unfamiliar stall due to the use of local produce.

Locally grown food will not be able to compete solely by virtue of having been grown in Singapore and would need to prove itself in terms of taste or price.

Join me next week where Mr James Kwan, Chief Marketting Officer of Barramundi Asia, shares his insights on some of the success and challenges they have faced so far.

Hi everyone, welcome back. As mentioned in the last blog post, I conducted a survey at the start of September to get an idea about what my friends felt about food security.

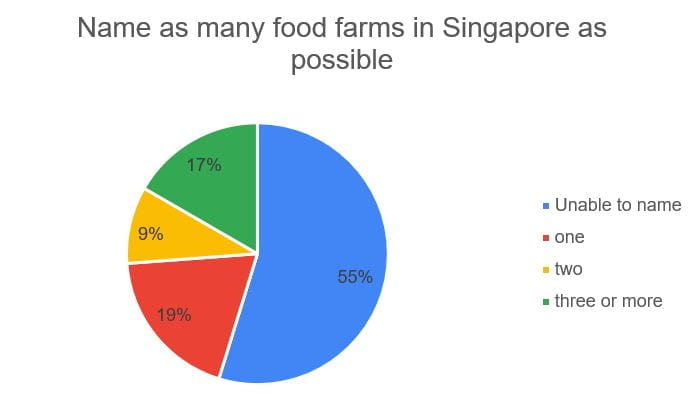

I realised that most respondents were not too familiar with the various local farms in Singapore. I asked respondents to list as many food farms as possible and vetted through their answers.

Most people could not name specific farms (although they were aware that Kranji/Lim Chu Kang had some and that there were fish, poultry and that one goat milk farm). This shows that the brand recognition of our local farms isn’t that high.

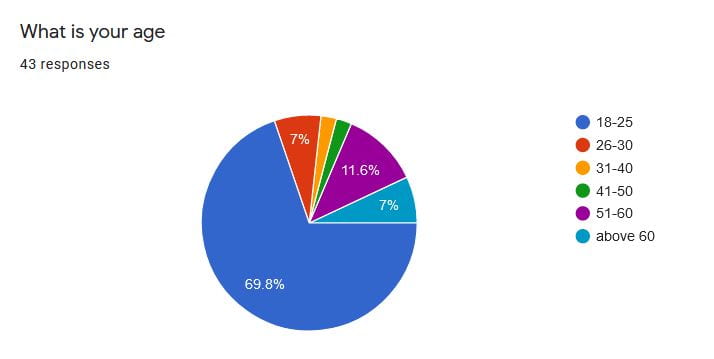

I looked back at the word cloud shown in last week’s post and realised that both “cheap” and “expensive” were commonly associated with local produce. I decided this warranted another survey and expanded the target audience to family and my hallmates.

Here is the breakdown of the demographics:

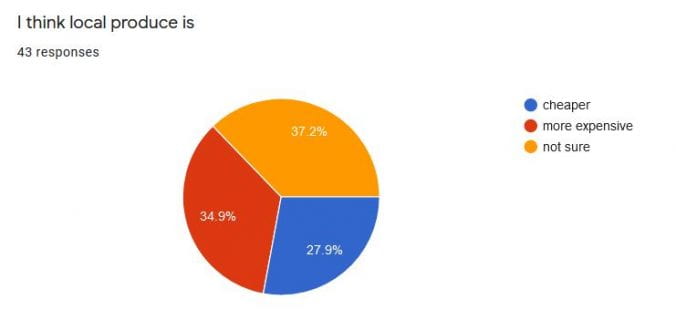

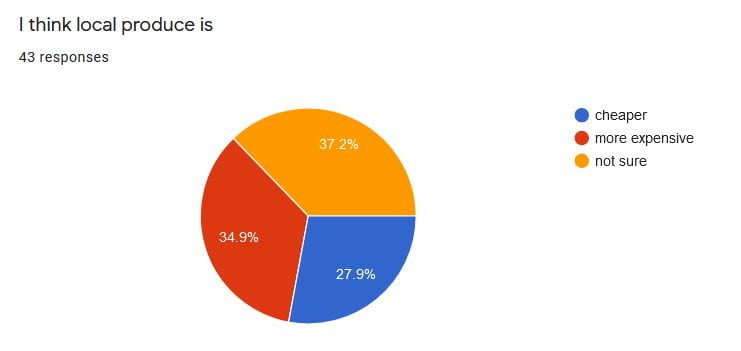

I asked respondents if they thought local produce was cheaper or more expensive. It appears that most of us were not sure, but fewer people thought that local produce was cheaper.

I avoided phrasing it as a agree/disagree question so as to not influence their answer, but “I think local produce is not sure” doesn’t make sense haha

Is this really the case? As mentioned in the last post, NTUC Fairprice carried more local produce than other supermarkets online. I compared local produce types on NTUC with imported produce from NTUC, Sheng Shiong and Red Mart, selecting the cheapest option for both local and imported produce, ignoring temporary offers. Here are my results:

Prices marked * are Pasar brand vegetables that are primarily sourced from Singapore but may use Malaysian produce to meet shortfalls. There is no difference in price between the local and Malaysian variants. I have included the next cheapest SGFP certified alternative if available.

Taugeh was a shoo-in and I struggled to find imports for that. It turns out that 70% of taugeh is grown locally. While our barramundi may be more expensive, we have a surprisingly large number of suppliers of fresh and frozen versions. While the price difference in eggs may appear significant, this was because local brands did not carry the larger 30 – egg trays and most chose to differentiate themselves in terms of freshness and nutritional value. If local egg farms are aiming to portray freshness, it may not make sense to sell the larger variants at supermarkets that may take longer for the average consumer to finish. I suspect they do sell in bulk to stall owners instead. Moreover, at the point of writing the cheapest local egg sold is actually on discount at $0.35/100g (29.6% more expensive than imports) while being lower in cholesterol with added Vitamin E.

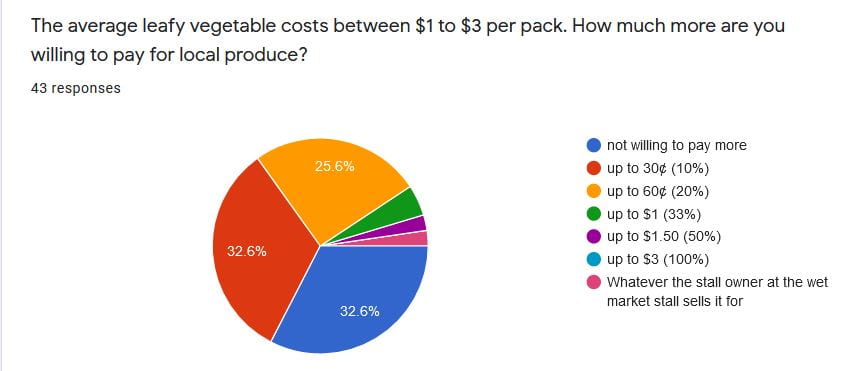

While there are cheaper imported leafy vegetables, the price difference is minimal. In fact, more than two-thirds of respondents were willing to pay up to 10% more for local produce.

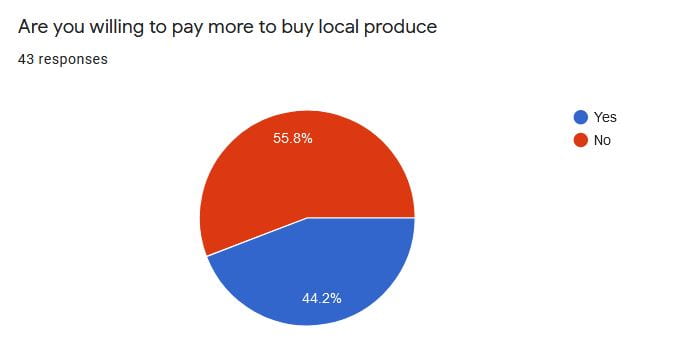

What’s interesting is that originally 44% of respondents were in principle unwilling to pay more before I quantified the price difference.

So, while local produce may not necessarily always be cheaper, the price difference is minimal and may be made up by the difference in quality such as freshness.

As we can see, when it comes to food, price is not the sole determinant. In conclusion, local produce can be competitive with imports even at the current price levels.

Through the course of these two posts, I’ve identified a few limitations with the SG Fresh Produce scheme. I’d be wrapping up this “trilogy” next week!

1971 Singapore 5 cent coin collected by this blogger.

Now this was in 1971 and was probably referring to capture fisheries instead of just aquaculture. As mentioned in slide 49 of today’s lecture, the percentage of biologically sustainable fish stocks was comfortably above 75% then.

So what has Singapore done to increase awareness of local food production? In February this year, SFA announced the launch the SG Fresh Produce (SGFP) logo that has been rolled out in August 2020.

Extracted from “Supporting Local Produce” https://www.sfa.gov.sg/food-farming/sgfoodstory/supporting-local-produce

This logo emphasizes that the food is local and fresh, and uses the “SG Brand mark” which is apparently the SG in a circle which has been used since the SG50 celebrations. This brand mark is also tied to the “Passion Made Possible” slogan, which has been our tourism slogan since 2017. Those in GE1101E this sem may be familiar with that…

Anyway, SFA has really been ramping up the exposure for this logo. I even chanced upon an advertisement just outside Kent Ridge MRT station!

This seems to be the main ad tying all the others together. They ran in a loop with other ads.

Beyond SFA, supermarkets have also started to roll them out. Here are screenshots of the online versions of Sheng Shiong and NTUC Fairprice:

I find Sheng Shiong’s online platform to be the more conducive of the two. Straight on the home page, shoppers get to view a category just for products farmed in Singapore with the SGFP logo displayed prominently.

Home page of Sheng Shiong’s online store, https://allforyou.sg/ retrieved 2 October 2020

SG Fresh Produces category, https://allforyou.sg/sg-fresh-produces retrieved 2 October 2020

In contrast, on Fairprice’s website, I first had to filter by item type then by country of origin (which is a great feature Sheng Shiong lacks) whereby I was directed to this page. I’m not too sure why some of the products featured here do not have the SGFP logo, perhaps they are undergoing certification.

NTUC online store, vegetables filtered by country of origin, https://www.fairprice.com.sg/category/fruits-vegetables?filter=Country%20Of%20Origin%3ASingapore retrieved 2 October 2020

As for the physical supermarkets, I have not noticed this sign much. Having to print collaterals as well as any necessary redesign of layout may take a while for each of their stores.

Personally, I quite like the SGFP logo. I find it refreshingly simple and to the point. Even though Passion Made Possible is not my favourite tourism slogan (and I’m sure quite a few of us did the GE1101E project on creating a new slogan), increasing it’s exposure to the local population will help to build a positive geographical image (lol) associated with it. It can also further solidify the SG Brand Mark, which was just announced last week. The brand mark is expected to be expanded to the local fashion and beauty sector soon.

The SGFP logo also highlights the key selling point of local produce, that of freshness. This seems to be in line with most of your expectations.

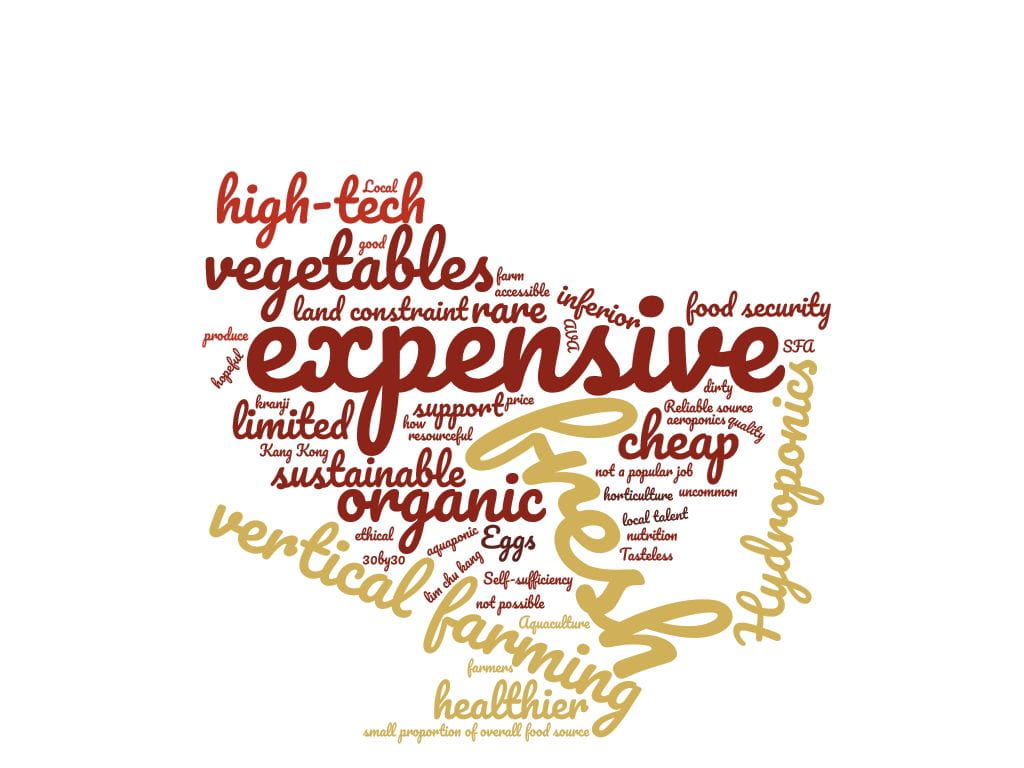

In a survey conducted at the start of this semester, I asked for your opinion of local produce. As can be seen in this word cloud, the main positive adjective associated is “Fresh”.

Word cloud regarding local produce

What were some of your thoughts regarding local food production? Stay tuned as I will be disclosing more of my findings next week!

Hi everyone, hope you had a fruitful recess week. We learnt about the current state of food production in Singapore last week. Keeping in mind that local food production is planned to meet only 30% of our nutritional demands, what are the strategies to ensure that the remaining 70% is secure?

The 30by30 plan is just one of three “food baskets” in Singapore’s food security strategy. Currently, “Diversify import sources” is the main way we maintain food security. SFA does this by certifying more supplier as safe for import while maintaining food safety standards. They also work with businesses in the industry to look for potential sources. Amidst the COVID 19 pandemic, Singapore has taken steps to ensure that food continues to reach Singapore. 12 countries including Singapore have signed the “Supply Chain Connectivity Agreements”, committing to keep the export of goods including food unimpeded.

Infomation collated from List of countries/regions approved to export raw and processed meat products, table eggs and processed eggs to Singapore (as at 10 Sep2020) retrieved https://www.sfa.gov.sg/docs/default-source/tools-and-resources/resources-for-businesses/approved-countries.pdf

It is interesting to note how varied our import sources for pork and poultry are. While the list is meant to be exhaustive, it seems to be missing Indonesia as an exporter of pork. Pulau Bulan, Indonesia has long been our sole source of fresh pork and it was just recently that pigs from Sarawak, Malaysia were allowed. I suspect this list omits live animals exported to Singapore for slaughter. I was surprised to learn that there is an abattoir in Singapore for this. Another unexpected absence is South Korea for beef. Upon further search, I realised that Korean marts selling cuts for KBBQs get their beef from Australia.

I am also surprised to see exporters of table eggs (unprocessed in shell form) being from as far away as Denmark. While it is great that we have a diverse range of exporters, I wonder how fresh the eggs can be once they reach Singapore and the carbon footprint involved for such a long journey.

It is reassuring to see that our food is imported from different regions around the world which would minimise the damage if a particular region had food production curtailed by environmental, political or health reasons.

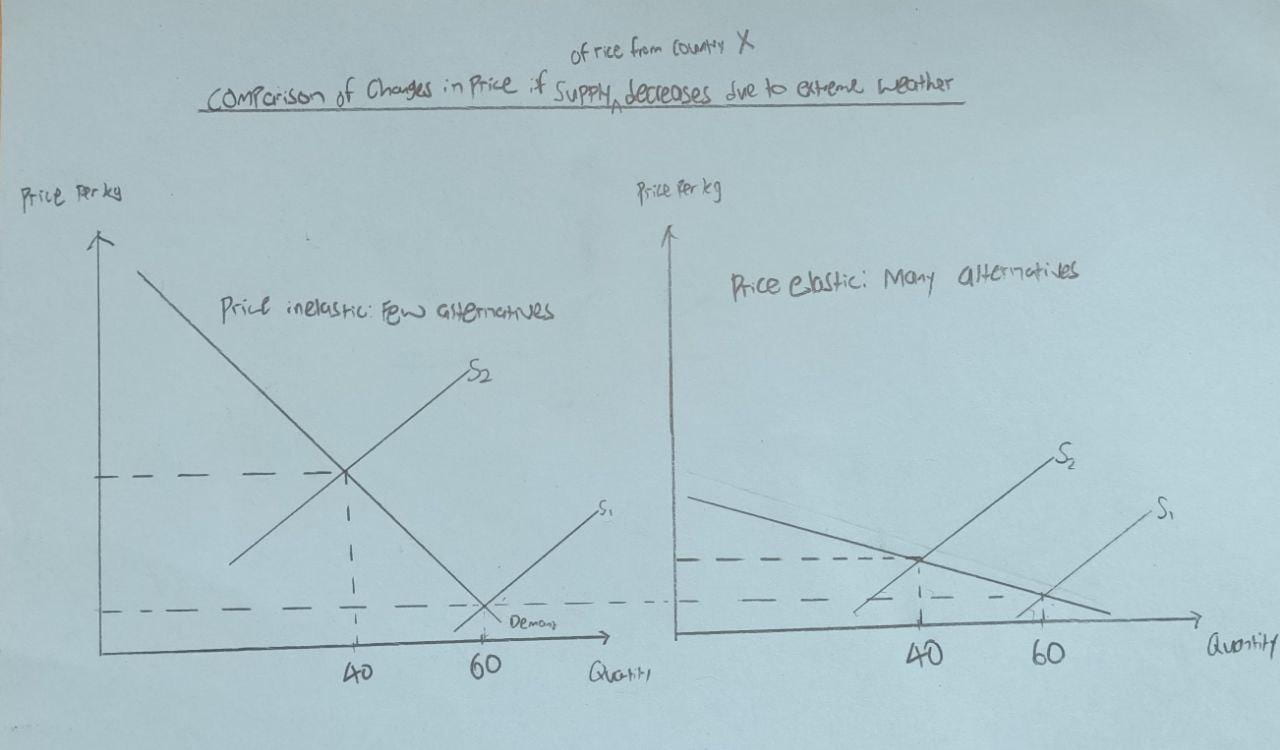

While diversifying food sources helps to protect us from supply shocks affecting one exporter, it also plays a role in keeping prices stable.

This author definitely isn’t trying to use this as an opportunity to revise for the upcoming Econs Mid-terms. As BES is a multi-disciplinary programme, it may be useful to think about how the different modules are related.

In this example, we consider a situation where Thailand experiences drought and supply of Thai rice falls. Luckily, Singapore has alternatives to rice from Thailand. Knowing that the importer has many alternatives, exporters will be less willing to artificially inflate their prices. This keeps food prices more stable.

SFA also encourages farms to expand overseas via the ‘Grow Overseas’ strategy. This allows local firms to have space and labour unavailable in Singapore to innovate and develop better methods. It will also be easier to import from these overseas ventures. Singapore also cooperates with the other governments, such as through the Singapore-Sino Jilin Food Zone, ensuring that food is exported to Singapore.

What are your thoughts on our trading partners, did any surprise you? What do you think about the grow overseas strategy, should it be considered a separate food basket midway between “grow local” and “diversify import sources”? Let me know in the comments!

Cheers and all the best for your submissions and midterms,

Hi everyone, welcome back 🙂 For a quick recap, we learnt about the agriculture scene in Singapore since the 40s, and how food security is not a new concept.

So where does that bring us today? Before I started this blog, I did a quick survey about what my friends (around three quarters were BES course mates) knew about food security.

Seems like we all have a lot to learn!

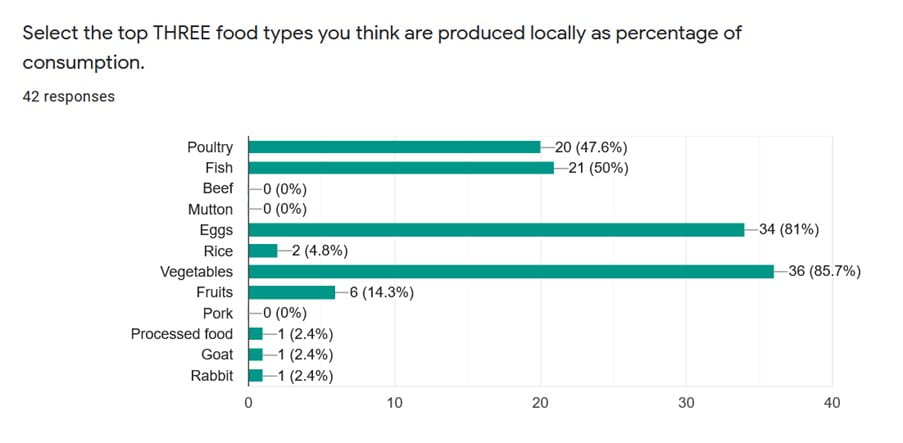

While most of us were reasonably sure about eggs and vegetables, a significant percentage of people were unable to identify what else Singapore produced.

Currently, a quarter of eggs, a tenth of fish, and 14% of leafy vegetables consumed in Singapore are grown locally. Of all 220 farms, 77 farms grow leafy vegetables, 121 farm fish (of which 109 are offshore) and just 5 produce eggs. I find it interesting that eggs, which we are most self-sufficient, have the least number of farms. This is especially noticeable when compared to fish farms. Is there a need for the consolidation of fish farms in the immediate future to achieve economies of scale? There certainly is room for cooperation. In 2015, waters off Pasir Ris were affected by algal bloom. Less affected farms took mitigation measures early, such as by temporarily transferring fish to farms in other areas. Larger farms with branches in different areas may be better able to handle these transfers at the first sign of trouble. It is also not as if fish farming is still in its infancy in Singapore. As early as 1984, “marine cage net fish farms” were in operation and accounted for 2% of fish consumed locally. If consolidation is not possible, fish farms could look into forming some sort of consortium which facilities cooperation and risk-sharing. After all, algal blooms are expected to be more common due to climate change and other anthropogenic reasons (Gobler, 2020). On the other hand, there are also risks to having just a small number of large companies. Should one company close due to financial mismanagement, local supply will be heavily affected. Of course, eggs and fish are very different products and it may not be possible to compare their markets quantitively.

It is also interesting that only half the participants surveyed identified fish as the top 3 products. I suppose this could be because most farms are offshore and barely noticed by Singaporeans. Moreover, fish are often sold without much information other than price and name.

Fish sold at my local supermarket

There is little information about their origin, unlike eggs and supermarket vegetables which at the very least have the farm’s name on it. Certainly, more can be done to highlight local produce when it comes to seafood.

barramundi of unknown origin sold at my local supermarket

Is this barramundi farmed in Singapore or imported? Nobody knows.

What are your thoughts on the number of fish and egg farms as compared to the percentage supplied locally? Let me know in the comments.

“To understand the present and anticipate the future, one must know enough of the past. Enough to have a sense of the history of the people. One must appreciate not merely what took place but more especially why it took place and in that particular way. That is true of individuals, as it is for nations”

—Lee Kuan Yew, during the PAP’s 25th Anniversary Rally, 1980

In the previous post, we learnt about the 30by30 goal. Before we think about how this goal can be achieved, let us know more about the context of food production in Singapore. How was the farming scene like, and how did the idea of food security come about?

The Japanese Occupation of Singapore was a very trying time. Growing up, I heard stories of my grandparents growing tapioca for sustenance. What was the “new normal” once the war ended? Here’s what I understand (from Chou 2014 ) about the local farming situation from the post-war years. Most farms were family-run. Being smaller, these farms were better able to react to changes in the market as compared to commercial ones. Such farms were able to meet local needs up to the 80s. However, pig farms were relocated to Punggol in the 70 due to concerns that wastewater would affect local water catchments (Tortajada et al, 2013).

However, 1984 marked a change in the government’s priorities (Tortajada & Zhang, 2016). In line with the transition to a knowledge-based economy, Primary Production Department Director, Mr. Goh Keng Swee, announced that Singapore no longer aimed to be self-sufficient for food. Instead, Singaporeans should specialise in areas higher up the value chain and rely on trade to meet other needs. The last pig farms in Punggol closed in 1989. Many areas involved in farming were converted into agrotechnology parks. Through these parks, modern farms can adopt each other’s best practises and technology more easily, resulting in higher and more sustainable yield.

Author at an agrotechnology park in 2006. Unfortunately, the only pictures I have are from that field trip when I was seven.

So what changed since 1984 that raised the importance of food security?

In 2007, there was a global food crisis. Due to drought and the shift to biofuel production, food prices rose dramatically leading to panic buying. The government highlighted that there was a national stockpile of rice – this was brought up again this year.

My biggest takeaway from the history of the food supply in Singapore is the importance of the government’s direction. 1984 showed that a decision to end self-sufficiency is a lot easier than efforts to raise it since 2007. The government needs to be clear what the goal is post-2030. T Ambiguity will only result in farmers hesitating to seize opportunities due to fears of being left in the lurch as pig farmers were back in the late 80s.

I understand why pig farming was phased out in the 80s. There was a risk that farmers would be left behind in Singapore’s march towards progress, creating a rural-urban divide. As they say, you can’t make an omelette without breaking a few eggs. Had the status quo been kept, the agriculture scene in Singapore may not have evolved into the technologically intensive scene we have today. It is also not fair to say that we could have maintained our sufficiency in pork as our population has almost doubled since then. However, keeping some sort of target for food sufficiency in mind would have been good. In hindsight, given the importance attributed to water security, the laissez-faire approach to food security seems out of character.

What do you think about the decision to shift away from self-sufficiency in the 80s? Was it a misstep, or was it more important that all Singaporeans shifted to jobs further up the value chain? What are your thoughts on the number of fish and egg farms in relation to the percentage supplied locally? Let me know in the comments.

Tortajada, Cecilia, and Hongzhou Zhang. “Food Policy in Singapore.” Reference Module in Food Science, 2016, doi:10.1016/b978-0-08-100596-5.21083-4.

Chou, Cynthia. “Agriculture and the End of Farming in Singapore.” Nature Contained: Environmental Histories of Singapore, by Timothy P. Barnard, NUS Press, 2014, pp. 216–240, muse-jhu-edu.libproxy1.nus.edu.sg/chapter/1096622.

Taiganides, E. P. Pig Waste Management and Recycling: the Singapore Experience. International Development Research Centre, 1992.

Recent Comments