“Be woke and conscious about how we can all be more sustainable and live in greater harmony with nature.”

– James Kwan, Chief Marketing Officer, Barramundi Asia

Hi everyone, welcome back. While we have examined the 30by30 plan so far, this has been mostly from the viewpoint of a consumer. There may certainly be blind spots we don’t know about, and nothing beats the experience in the industry. On the 12th of October, I had the privilege to interview Mr James Kwan, Chief Marketing Officer of Barramundi Asia. Barramundi Asia is the parent company of Kühlbarra – a local barramundi farm – and UVAXX – which oversees fish health.

Here are the highlights of our interview as well as my thoughts. The transcript of our phone interview can also be found here.

Q: Your farm is currently the only one situated in deeper waters. Why has Barramundi Asia taken this unique approach, and why isn’t this more common?

A: In South East Asia, the traditional and primary form of aquaculture production has largely been kelongs. While kelongs are tried and tested, and suitable for artisanal volumes; intensive aquaculture requires deeper ocean waters with strong currents to ensure low stocking densities and disease mitigation and ultimately healthier, and happier fish. For Barramundi Asia, we have adopted methods from the global industrial salmon aquaculture for barramundi, where we use large and deep sea cages…(depths of around 20 metres and a diameter around 25-30 metres). These nets allow large volumes of water, and when carefully stocked with the correct biomass, are optimal for growth and animal health. This mode of aquaculture is typically more capital and investment heavy, as they require surface support and harvest vessels, floating living quarters, feed storage, dive operations…etc, which is probably why we are one of the few in Asia that adopt this method.

Q: Are there any concerns about water quality given your open net system? Are harmful algal blooms (HAB) a concern?

Water quality in aquaculture is always a priority and challenge, whether you are culturing in a land-based pond, lakes or in shallow-based kelongs or out in the open ocean. This is precisely why as a farm we sited our farm in the southern waters of Singapore because of the strong oceanic currents. There are multiple environmental factors that make HAB events more likely…by situating our farm in waters that have strong currents, high dissolved oxygen readings, and away from potential agricultural nutrient pollution sources and outfalls, we mitigate these risks significantly. I distinctly remember the afternoon in 2015 when our northern farms along the Johor Strait experienced a HAB that wiped out 600 tons of fish biomass; I was diving a cage with a prominent local French chef who had dropped by to see how we farmed in deep waters. We talked about the importance of surveillance and HAB forecasting, so that farms are able to be prepared for any eventuality. Unlike kelongs, we could technically un-moor our cages and tow them away from affected waters if necessary.

Apart from the measures mentioned, I think that it is also important that SFA works with industry players to seek their input and experience when it comes to formulating guidelines and licensing agreements. With the rather nascent aquaculture scene in our southern waters, farm operators would have the most experience when it comes to on-site conditions. Taking the more crowded northern waters into account, factors such as oxygen demand should be considered in the future. These operators also stand to benefit from being able to have their voices heard. While some people may be suspicious of any cooperation between the government and corporations, I think that the knowledge industry players bring is irreplaceable. Of course, there is always space for evidence-based policymaking through studies of site conditions, but that may take a bit more time and research funds.

Q: Why did your company choose to specialise in Barramundi? I notice that Kühlbarra also offers salmon. Are there plans to farm other fish?

A:There are many reasons why barramundi was chosen. As we are situated in the tropics, we had to find a viable species that would meet the requirements of fast growth, disease resilience, optimal feed to protein conversion, and market acceptance. Barramundi (sp. Lates calcarifer) is particularly suitable also because it can be acclimatised to pellet feed. where we are able to then tailor nutritional and sustainable components to the feed. The feed that we use is 70% plant base, with a very low FCR (feed conversion ratio), which ultimately makes our barramundi, arguably the most sustainable premium white fish in the market.

We sell salmon on our online store as an added value-add to our customers who may also want salmon. Many of our management team come from the salmon aquaculture industry and have strong ties with producers around the world, allowing us to bring in fresh salmon regularly.

I think this is really eye-opening. It is great that the fish can be fed pellets, which are less pollutive and less likely to spread disease as compared to other methods such as trash fish. The use of vegetable proteins as opposed to the meat or fish-based ones also mean a lower carbon footprint, making it more sustainable overall.

Q: It is estimated that half of your production is sold locally while the rest is exported. Is local demand not high enough, or are there other benefits to exporting your products?

A: As a business, we need to look into all markets to ensure financial sustainability. But as Singapore’s largest aquaculture producer, we of course prefer to focus on local demand.

While the market can absorb more fish from our farm, we offer a product that is produced towards the highest standards and that obviously comes with a cost. We are one of a handful of BAP( Best Aquaculture Practice) certified facilities in the region; and the only in Singapore. We use only 100% traceable, sustainable feed, monitor our water quality and maintain assure customers of 100% chain of custody of our fish from farm to fork. So while we see more local consumers beginning to demand for better quality, certified farmed fish, the volume we produce is sold offshore to more developed markets where customers only want traceable and sustainably produced fish.

For example, in Australia, our farm in Western Australia produces fish that are sold to Coles supermarket chain, with around 800 stores around the country. In the US or across certain international hotel chains, our products are selected because we are able to produce to the standards required. In Singapore, you can find us in Cold Storage, RedMart or through our online portal at kuhlbarra.com.

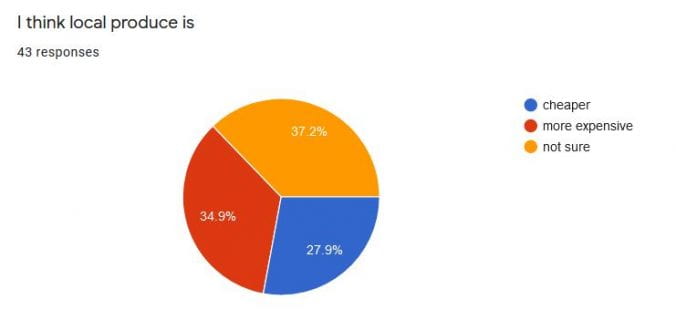

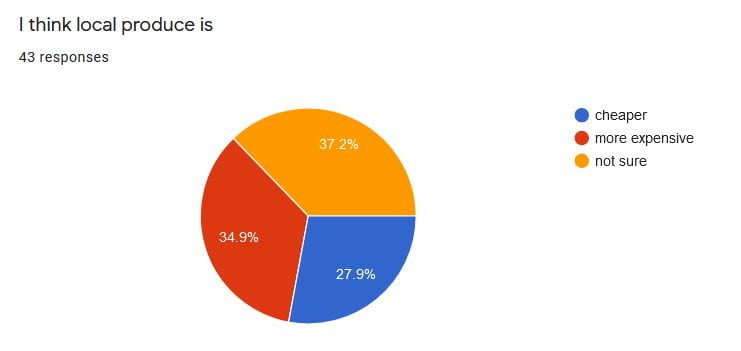

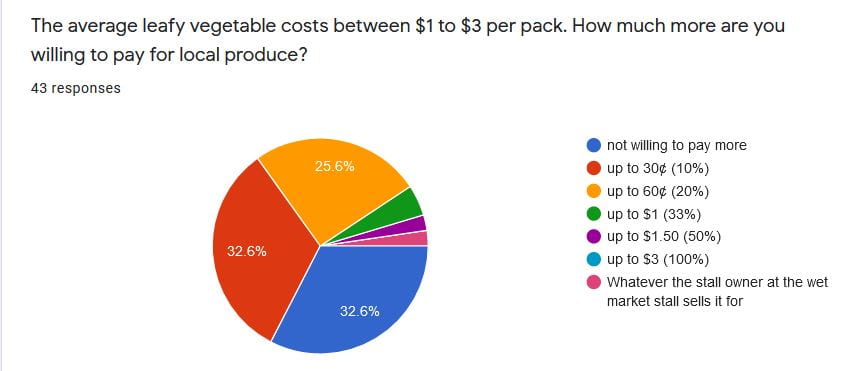

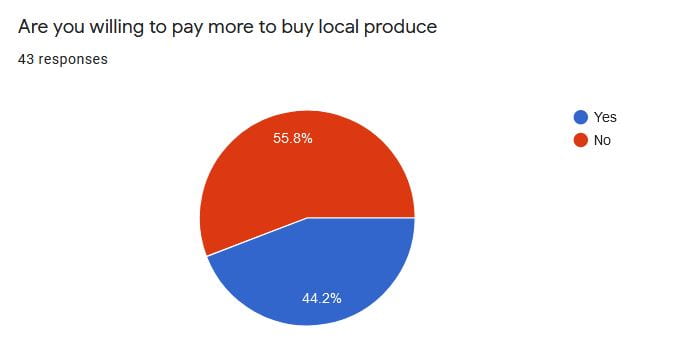

As shown in my survey results from the previous post, Singaporeans are not just price-conscious but also pay attention to taste and quality. It is logical for local farms to focus on their freshness and taste – and it has evidently served Kühlbarra well. It might also be harder to compete with cheaper fish from less sustainable farms in the region. Anecdotal evidence in the comments section suggests that there is some baseline level of demand, even if they may be more pricey.

Image by Eleanor Loh/ Steamed Tiberias Barramundi from the Open Farm Community. Personal photograph reproduced with permission.

I’ve tried locally farmed barramundi at the Open Farm Community restaurant, and it tasted pretty good. However, at that price point if we weren’t there for a celebration I may not have gone. With the recession caused by the COVID pandemic, people may become more price conscious too.

Q: Your products are vacuum sealed for freshness and delivered in styrofoam boxes. How will the Resource Sustainability Act affect you and what measures are being considered to reduce waste?

A: As our business extends past just aquaculture and into fish and food processing, we are very much committed to working towards zero waste solutions. However, as we mainly deal with a fresh product, we do need to rely on IVP (individually vacuum packaging) to ensure food safety. We transport some of our products in EPS boxes to ensure cold-chain integrity for food safety. Despite the limitation of Expanded Polystyrene (EPS) densification and recycling facilities within Singapore, we believe that EPS’ benefits far outweigh its cons in terms of its insulative performance. To mitigate this, we do have a return policy for our polystyrene boxes where the delivery agent retrieves it during the next delivery. Recycled boxes are brought back to our factory and disinfected with food grade alcohol. We are also exploring hybrid paper based IVP primary packaging, working with international customers on their requirements. At the end of the day, it is a multiprong strategy that involves our customers too.

In terms of sustainability and waste management, we are also looking at employing ensilage systems in 2021 to ensure that food trimmings, mortalities and other biological waste are treated within our own company, with end products potentially sold downstream to feed or fertiliser companies.

Now, this is where the 30by30 goal may not necessarily bode well for the environment. By emphasising freshness, certain single-use packaging may come into play. How many people would be willing to have fish delivered in an insulative box and handed over without any packaging? As I learnt during an online seminar on the Resource Sustainability Act, vegetable farms also grapple with the issue of plastic packaging for veggies delivered to supermarkets. It would be interesting to compare that with groceries bought from neighbourhood markets, where fish and vegetables are displayed without packaging. If anything, producers may be responsive to consumer feedback when it comes to packaging.

Once again, I’m thankful for James to take the time for the insightful interview and to his team for vetting through the transcript.

We talked a lot more – which I do not have the space to elaborate on. It’ll be appended at the end for your perusal.

Cheers,

Ee Kin

Q: Has COVID-19 affected your plans to triple production by 2022?

A: Definitely all farms around the world are affected. For us, as travel restrictions came in place and the Aviation and HORECA (HOtels, REstaurants, CAtering) industry got devastated, so did B2B orders for our fish. Thankfully, as we have a relatively robust online presence well established, and a loyal following, we saw an uptake in our online sales by over 3x as the Circuit Breaker came in place. Despite this, we have made the necessary changes in our business and production to meet our 2022 volumes despite the severe impact of COVID.

Q: How does the 30by30 plan to increase food production affect you? Are there areas in current measures that you feel could be improved on?

A: As a Singaporean company with global ambitions, we believe and fully support the government’s initiative towards our 30×30 Food Security goals. It doesn’t affect us per se, but in fact has spurred our team on as we believe that Singapore, as unlikely as it is, can be a global aquaculture player, and a country that can further strengthen our already strong food security framework. It is fantastic that more Singaporeans are now aware of the importance of supporting local produce, which has been put in the spotlight during Covid.

For the SG produce logo, I remember voting for my preferred design earlier this year. I think it is a great start to start branding and recognising al local farmers. Perhaps apart from informing Singaporeans about the existence of a vibrant local food production sector, it hopefully inspires more of our young Singaporeans to participate and join this exciting sector.

Q: How do your Kimberly site in Australia and the upcoming site in Brunei benefit food production in Singapore?

A: Recently, the government has highlighted this through the “game change food security” advertisements. I believe we are the only Singaporean company that has taken production abroad. The government has supported us tremendously and we believe in their vision that food security and production need not be constraint to within national borders. By investing in Singapore companies that can produce outside of our shores, we add an additional dimension and strength to an already strong Food Security framework.

authors note: Check out SFA’s website on the latest updates on the Grow Overseas strategy.

Q: Can you comment on the relations with other fish farms in Singapore? Is it a close-knit community or do farms generally operate independently?

A: Farmers do operate independently, and are still loosely associated in Singapore. In the coming years, we hope to see greater interaction. Of course, we would like to think we have a great relationship with all other farmers! (laugh). Farming is somehow a primal activity and that alone makes us more understanding and sympathetic to one another’s challenges. As the largest and most resourced farm in Singapore, we do want to share or expertise and experience with those who are willing to listen. However, as our method of production with large ocean nets and deep waters are different from every other farm in Singapore, I guess there is knowledge that are not quite transferable. At Barramundi Asia, we are not just farmers, but a congregation of marine biologists, animal health and husbandry specialists and veterinarians. So we do feel for every other farmer, say when they were hit by the HAB in 2015. As an animal lover, we were all sick to the gut when we realised how many animals were affected. Recently, as part of our CSR and efforts to give back to the industry, our wholly-owned, sister company and hatchery, Allegro Aqua, just donated fingerlings to a farm in the north. We also sell this fast growing fry and fingerlings that are disease-resistant to other farms. An ST journalist was present and I believe it will be covered by the Straits Times soon.

Q: Is there anything else you want to tell our readers?

A: It’s important to eat local, support local. Know what you are eating….know what went into the animal you ate and how it was farmed and harvested. Be woke and conscious about how we can all be more sustainable and live in greater harmony with nature.

Recent Comments